For panel beating repairs under R5,000, paying cash is almost always cheaper than claiming from insurance once you factor in premium increases (10–20% per year for 3+ years) and loss of your no-claims bonus.[1] For repairs over R8,000, claiming usually makes financial sense. The grey zone between R5,000 and R8,000 depends on your specific excess, premium, and claims history.

Key Takeaways

- Under R3,000 repair: almost always pay cash

- R3,000–R8,000: compare your excess + 3 years of premium increases vs repair cost

- Over R8,000: claiming usually makes sense

- Hail damage: always claim (act of nature, minimal premium impact)

- Not-at-fault claims: always claim (insurer recovers from responsible party)

Understanding Insurance Excess

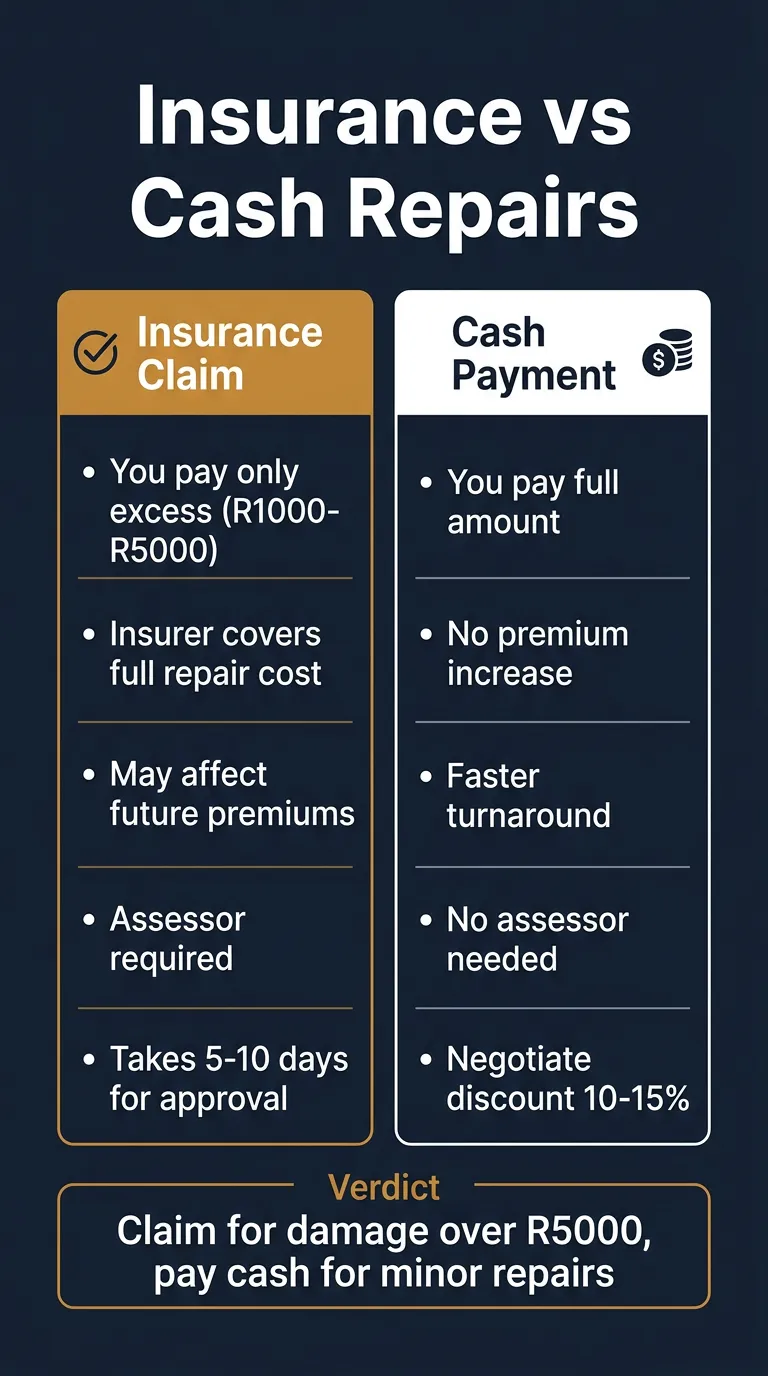

Your insurance excess is the amount you pay out of pocket before your insurer covers the rest. In South Africa, this typically ranges from R3,000 to R7,000 for standard motor policies[1], though it can be higher for younger drivers, high-risk areas, or specific vehicle categories.

Some policies have additional excess structures:

- Basic excess — the standard amount on all claims

- Voluntary excess — an additional amount you agreed to in exchange for lower monthly premiums

- Age-related excess — extra excess for drivers under 25 (often R3,000–R5,000 on top of the basic excess)

Before deciding whether to claim, you need to know your total excess amount. If your excess is R5,000 and the repair costs R6,000, you're only getting R1,000 of benefit from the claim — and the downstream costs may outweigh that.

The Hidden Cost of Insurance Claims

Filing a claim doesn't just cost you the excess — it can affect your premiums and benefits for years:

Premium Increases

Most South African insurers adjust premiums based on your claims history. A single at-fault claim typically increases your premium by 10–20% at renewal.[1] Two claims within a short period can push increases to 30% or more. Over a 3–5 year period, the cumulative premium increase on a policy costing R1,500/month can easily total R5,000–R15,000 in additional costs.

Loss of No-Claims Bonus

Many policies offer a no-claims discount (also called a loyalty bonus) that accumulates over claim-free years — typically 10–20% off your premium. Filing a claim resets this, effectively increasing your costs even beyond the direct premium adjustment.

When to Claim: Insurance Makes Sense

- Repair cost significantly exceeds your excess — if the repair is R15,000 and your excess is R4,000, the R11,000 of cover is substantial.

- Major collision damage — collision repairs costing R20,000–R50,000+ are exactly what insurance is designed for.

- Not-at-fault claims — your insurer recovers costs from the responsible party. This typically doesn't affect your premiums.

- Hail damage — most insurers treat these as "act of nature" claims, which often don't penalise your claims history.

- You need a rental vehicle — if your policy includes car hire benefit, claiming gives you access to a rental while your car is being repaired (worth R3,000–R10,000).

When to Pay Cash: Out-of-Pocket Makes Sense

- Repair cost is close to your excess — claiming R1,000 benefit while facing years of premium increases is poor maths.

- Minor cosmetic damage — small dents, light scratches, and bumper scuffs often cost R1,000–R3,000 to repair. Well below most excess amounts.

- You've recently had another claim — a second claim in quick succession can trigger significant premium increases or even non-renewal.

- You value your no-claims bonus — if you've built up a significant discount, preserving it may outweigh the claim value.

Insurance vs Cash: Side-by-Side Comparison

| Factor | Insurance Claim | Cash Payment |

|---|---|---|

| Upfront cost | Excess only (R3,000–R7,000) | Full repair cost |

| Long-term cost | Premium increase 10–20%/yr for 3+ years | None |

| Turnaround time | +3–7 days for authorisation | Work starts immediately |

| Parts used | OEM specified by insurer | Choice of OEM or quality aftermarket |

| Paperwork | Claim forms, assessor visits, authorisation | Quote, approve, pay |

| Rental vehicle | Available if policy includes car hire benefit | Not included |

| No-claims bonus | Lost or reduced | Preserved |

The Break-Even Calculation

Here's a practical framework for deciding. You'll need three numbers:

- Repair cost — get a quote from a reputable panel beater in Centurion

- Your total excess — the amount you'd pay out of pocket on a claim

- Estimated premium increase — roughly 15% of your annual premium for a single claim

The Formula

If (Repair Cost - Excess) > (Annual premium increase x 3 years), then claiming makes financial sense. If the claim benefit is less than the cumulative premium increase, paying cash is usually better.

Example: Repair costs R8,000. Excess is R4,000. Monthly premium is R1,200 (R14,400/year). A 15% increase = R2,160/year, or R6,480 over 3 years. Claim benefit is R4,000 (R8,000 minus R4,000 excess). Since R4,000 < R6,480, paying cash is the better decision.

The Smart Approach: Claim Big, Pay Small

The most financially savvy approach is to use insurance for what it's designed for — significant, expensive damage — and pay cash for minor repairs. This preserves your claims history, keeps premiums low, and still protects you from catastrophic costs.

| Repair Cost | Recommendation | Reason |

|---|---|---|

| Under R3,000 | Pay cash | Below most excess amounts |

| R3,000 – R8,000 | Calculate carefully | Depends on excess and premium |

| Over R8,000 | Claim | Benefit exceeds long-term cost |

| Hail damage | Always claim | Act of nature, minimal premium impact |

| Not-at-fault | Always claim | Costs recovered from responsible party |

When in doubt, get a repair quote first and then call your insurer to ask about the specific premium impact. A trustworthy workshop that handles insurance claims will also give you honest advice about whether a claim is worthwhile for your particular repair.

Sources

- AA South Africa — Vehicle insurance advice, excess structures, and claims guidance

- MechanicBuddy.co.za — Real panel beating quotes for cash vs insurance comparison

- SAMBRA (South African Motor Body Repairers' Association) — Consumer rights and insurance claim guidance

- AutoTrader South Africa — Repair cost baselines for insurance vs cash decisions

Frequently Asked Questions

Can I claim panel beating from insurance?

Yes, if you have comprehensive motor insurance in South Africa, panel beating for accidental damage is covered. You'll pay your excess (typically R3,000–R7,000), and the insurer covers the rest. Third-party-only policies do not cover damage to your own vehicle. You have the legal right to choose your own panel beater.

Is cash panel beating cheaper than insurance?

The repair itself may be slightly cheaper as cash because workshops have more flexibility with parts. However, the real saving from paying cash is avoiding insurance premium increases (typically 10–20% per year for 3+ years after a claim) and preserving your no-claims bonus. For repairs under R5,000, cash is often the better financial decision.

Will my insurance premium increase if I claim for panel beating?

In most cases, yes. At-fault claims typically increase premiums by 10–20% at renewal. Multiple claims can trigger 30%+ increases. However, not-at-fault claims and act-of-nature claims (hail damage) may have less or no impact — check with your specific insurer.

Can I choose my own panel beater for an insurance claim?

Yes. In South Africa, you have the legal right to choose your own panel beater for insurance repairs. Your insurer may recommend their preferred network, but they cannot force you to use a specific workshop.

How much is the insurance excess for panel beating?

Standard motor insurance excess in South Africa ranges from R3,000 to R7,000. Some policies have additional voluntary excess (chosen by the policyholder for lower premiums) or age-related excess for drivers under 25. Check your policy schedule for your specific excess amount before deciding whether to claim.

![Bumper Repair Cost in South Africa: Repair vs Replace [2026]](/images/hero-bumper.webp)